FinRL is the open source library with a unified framework for practitioners for pipeline strategy development. In reinforcement learning (or deep RL), an agent learns by interacting with an environment, in a trial and error manner, achieving a balance between exploration and exploitation. The open source community AI4Finance (to efficiently automate trading) provides educational resources to learn about deep reinforcement learning (DRL) in quantitative finance.

To contribute? Please check the call for contributions at the end of this page.

Feel free to report bugs using Github issues, join our mailing list: AI4Finance, and discuss FinRL in the slack channel:

Roadmaps of FinRL:

FinRl 1.0: entry-level toturials for beginners, with a demonstrative and educational purpose.

FinRl 2.0: intermediate-level framework for full-stack developers and professionals.

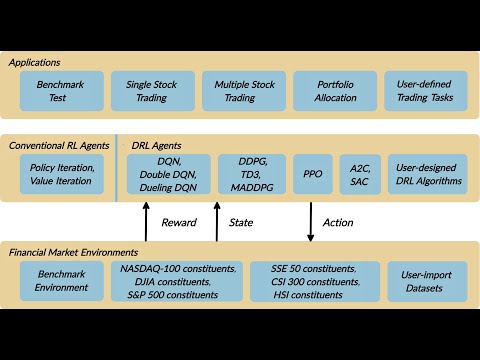

FinRL provides a unified machine learning framework for various markets, SOTA DRL algorithms, benchmark finance tasks (portfolio allocation, Cryptocurrency trading), live trading, etc.

We published papers in FinTech and now arrive at this project:

4). FinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance, Deep RL Workshop, NeurIPS 2020.

3). Deep Reinforcement Learning for Automated Stock Trading: An Ensemble Strategy, paper and codes, ACM International Conference on AI in Finance, ICAIF 2020.

2). Multi-agent Reinforcement Learning for Liquidation Strategy Analysis, paper and codes. Workshop on Applications and Infrastructure for Multi-Agent Learning, ICML 2019.

1). Practical Deep Reinforcement Learning Approach for Stock Trading, paper and codes, Workshop on Challenges and Opportunities for AI in Financial Services, NeurIPS 2018.

[Towardsdatascience] FinRL for Quantitative Finance: Tutorial for Single Stock Trading

[Towardsdatascience] FinRL for Quantitative Finance: Tutorial for Multiple Stock Trading

[Towardsdatascience] FinRL for Quantitative Finance: Tutorial for Portfolio Allocation

[Towardsdatascience] Deep Reinforcement Learning for Automated Stock Trading

[Analyticsindiamag.com] How To Automate The Stock Market Using FinRL (Deep Reinforcement Learning Library)?

[量化投资与机器学习] 基于深度强化学习的股票交易策略框架(代码+文档)

[Neurohive] FinRL: глубокое обучение с подкреплением для трейдинга

A YouTube video about FinRL library. [YouTube] AI4Finance Channel for quant finance.

We implemented Deep Q Learning (DQN), Double DQN, DDPG, A2C, SAC, PPO, TD3, GAE, MADDPG, InterSAC, InterAC, MuZero, etc. using PyTorch and OpenAI Gym.

Version History [click to expand]

- 2020-12-14 Upgraded to Pytorch with stable-baselines3; Remove tensorflow 1.0 at this moment, under development to support tensorflow 2.0

- 2020-11-27 0.1: Beta version with tensorflow 1.5

Clone this repository

git clone https://github.com/AI4Finance-LLC/FinRL-Library.gitInstall the unstable development version of FinRL:

pip install git+https://github.com/AI4Finance-LLC/FinRL-Library.gitBuild the container:

$ docker build -f docker/Dockerfile -t finrl docker/Start the container Note: The default container run starts jupyter lab in the root directory, allowing you to run scripts, notebooks, etc.

$ docker run -it --rm -v ${PWD}:/home -p 8888:8888 finrlFor OpenAI Baselines, you'll need system packages CMake, OpenMPI and zlib. Those can be installed as follows

sudo apt-get update && sudo apt-get install cmake libopenmpi-dev python3-dev zlib1g-dev libgl1-mesa-glxInstallation of system packages on Mac requires Homebrew. With Homebrew installed, run the following:

brew install cmake openmpiTo install stable-baselines on Windows, please look at the documentation.

cd into this repository

cd FinRL-LibraryUnder folder /FinRL-Library, create a Python virtual-environment

pip install virtualenvVirtualenvs are essentially folders that have copies of python executable and all python packages.

Virtualenvs can also avoid packages conflicts.

Create a virtualenv venv under folder /FinRL-Library

virtualenv -p python3 venvTo activate a virtualenv:

source venv/bin/activate

To activate a virtualenv on windows:

venv\Scripts\activate

The script has been tested running under Python >= 3.6.0, with the folowing packages installed:

pip install -r requirements.txtAbout Stable-Baselines 3

Stable-Baselines3 is a set of improved implementations of reinforcement learning algorithms in PyTorch. It is the next major version of Stable Baselines. If you have questions regarding Stable-baselines package, please refer to Stable-baselines3 installation guide. Install the Stable Baselines package using pip:

pip install stable-baselines3[extra]

A migration guide from SB2 to SB3 can be found in the documentation.

Still Under Development

python main.py --mode=trainUse Quantopian's pyfolio package to do the backtesting.

The stock data we use is pulled from Yahoo Finance API

(The following time line is used in the paper; users can update to new time windows.)

- FinRL is an open source library specifically designed and implemented for quant finance. Trading environments incorporating market frictions are used and provided.

- Trading tasks accompanied by hands-on tutorials with built-in DRL agents are available in a beginner-friendly and reproducible fashion using Jupyter notebook. Customization of trading time steps is feasible.

- FinRL has good scalability, with a broad range of fine-tuned state-of-the-art DRL algorithms. Adjusting the implementations to the rapid changing stock market is well supported.

- Typical use cases are selected and used to establish a benchmark for the quantitative finance community. Standard backtesting and evaluation metrics are also provided for easy and effective performance evaluation.

@article{finrl2020,

author = {Liu, Xiao-Yang and Yang, Hongyang and Chen, Qian and Zhang, Runjia and Yang, Liuqing and Xiao, Bowen and Wang, Christina Dan},

journal = {Deep RL Workshop, NeurIPS 2020},

title = {FinRL: A Deep Reinforcement Learning Library for Automated Stock Trading in Quantitative Finance},

url = {},

year = {2020}

}

We will maintain the open source FinRL library for the "AI + finance" community and welcome you to join as contributors!

This project exists thanks to all the people who contribute.

We would like to support more asset markets, so that the users can test their stategies.

We will continue to maintian a pool of DRL algorithms that can be treated as SOTA implementations.

To help quants have better evaluations, here we maintain benchmarks for many trading tasks, upon which you can improve for your own tasks.

Supporting live trading can close the simulation-reality gap, it will enable quant to switch to the real market when they are confident with their strategies.

MIT